First Choice Foods Pvt Ltd, based in Butwal, made history n June 2025 by exporting French fries to the United states–an unprecedented milestone for Nepal’s agri-processing sector. Buoyed by the breakthrough, the company is now preparing to enter the UK, Australian, and Japanese markets. Operating under the Himalayan Crisps brand, First Choice produces premium French fries and other potato-based products at its processing plant in Mainahiya, Rupandehi, serving both domestic and international customers. Its expansion has been supported by growth capital from Nepali private equity firm Avasar Equity.

A similar arc of scale and ambition is unfolding in technology. In October 2025, Fusemachines Inc. announced that its ticker had gone live on NASDAQ, becoming the first company founded by a Nepali-origin entrepreneur to be listed on the exchange. The listing marked a defining moment for Nepal’s IT sector, placing a Nepali-founded firm alongside global technology leaders. Fusemachines was backed at an early stage by Nepali private equity and venture capital firms Business Oxygen and Dolma Impact Fund, which helped it scale into a global enterprise AI company.

In consumer goods, Delish Diaries is reshaping Nepal’s dairy market with premium Greek yogurt made using traditional methods and high-quality ingredients. Revenues surged from Rs 90 million in fiscal year 2023/24 to Rs 220 million in FY 2024/25, enabling the company to break even and expand to three production plants. Its growth has been accelerated by Rs 115 million in Series A funding from NIBL Equity Partners. Likewise, Nepal’s leading food-delivery platform, Foodmandu, scaled nationally with backing from Nepali PE/VC firms True North Associates and Team Ventures.

Taken together, these trajectories mark a turning point. What once appeared episodic and externally driven is consolidating into a domestically anchored risk-capital ecosystem. In 2024, Nepal’s private equity and venture capital industry crossed a threshold that had been years in the making. For the first time, risk capital was no longer operating at the margins of the financial system; it was shaping it.

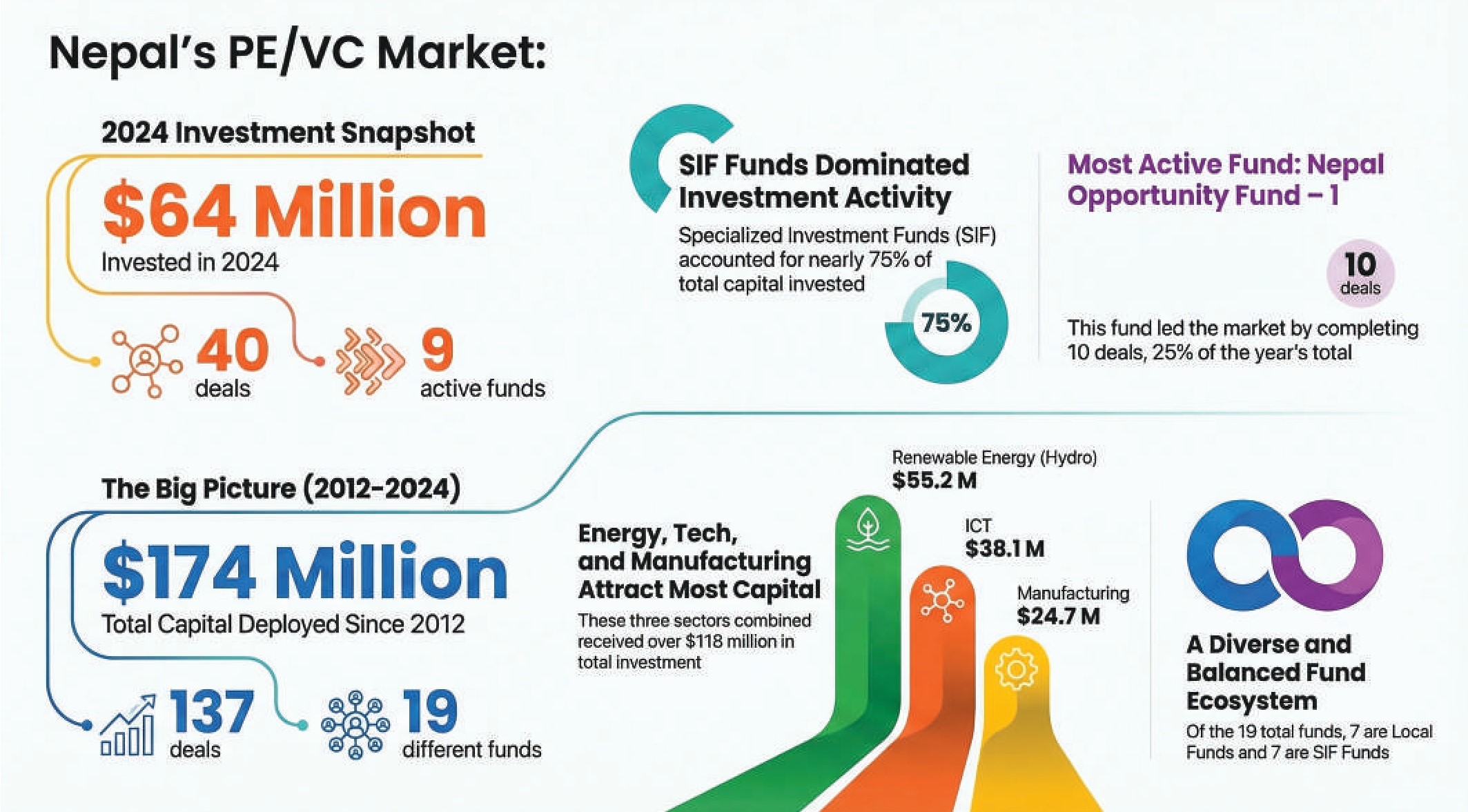

According to the Nepal Private Equity Association’s Market Intelligence Report, PE/VC funds invested $64 million in a single year—the highest annual deployment on record. That figure alone accounted for nearly 40% of all private equity and venture capital investment made in Nepal since 2012. Forty deals were closed during the year across nine active funds, three of which were deploying capital for the first time.

More telling than the volume, however, was the source. Over 74% of 2024 investments came from funds licensed under Nepal’s Specialized Investment Fund (SIF) framework. Across the 2012–2024 period, domestic capital—mobilized through both SIF and non-SIF local funds—now accounts for more than 57% of total PE/VC deployment. Risk capital, once largely imported through donor-led and offshore vehicles, is increasingly being generated—and recycled—at home.

This rebalancing carries implications far beyond deal counts. Nepal’s private equity and venture capital industry is emerging not as a substitute for banks, but as a structural complement to a bank-dominated financial system. In Nepal, access to bank credit is contingent on promoters first contributing substantial equity—yet for many entrepreneurs, mobilizing that equity has long been the binding constraint. Commercial banks do not finance ideas; they finance established enterprises with balance sheets, collateral, and predictable cash flows. Private equity fills the gap between concept and credit, providing the risk capital required to establish enterprises, meet debt–equity ratios, and ultimately make projects bankable.

In this sense, PE/VC does not displace banks; it enables them, expanding the universe of viable borrowers and investable projects. It signals a transformation in how capital is mobilized, how risk is shared, and how Nepali enterprises scale—moving the economy, at last, beyond an overwhelming dependence on banks, collateral, and personal guarantees.

Before the Labels Existed

Private equity did not arrive in Nepal with a regulatory framework or even a shared vocabulary. Long before the term entered policy documents, investment companies were already pooling capital, hiring professional managers, and taking stakes in businesses—particularly in energy and trading.

“If we look at the history of private equity in Nepal, before there was a formal PE/VC licensing regime, these activities existed mainly through investment companies,” says Manish Thapa of Global Equity Fund. “From around 2012, private equity and venture capital began to take shape in a more organized manner, but there was no regulation.”

In that early phase, the model was rudimentary. Capital was pooled, an investment company was formed, and funds were deployed across multiple sectors. Most early investments flowed into hydropower, with limited exposure to information technology. Governance standards varied widely, shareholder protections were inconsistent, and exits were rare.

What was missing was not capital alone, but a philosophy of shared risk, structured governance, and long-term partnership. That conceptual break came with the arrival of two institutions: Business Oxygen and Dolma Impact Fund. Backed by international development partners, they introduced ideas that were largely unfamiliar to Nepal’s private sector—minority equity, structured shareholder agreements, ESG standards, and the principle that investors share losses as well as gains.

“When Dolma Fund and Business Oxygen entered the market, private equity formally arrived in Nepal,” Thapa says. “They didn’t just invest capital; they established the very concept of private equity.”

Their emergence coincided with broader global changes. The rise of private equity in Nepal also coincided with a deeper transition in development finance itself. As Nepal moved toward middle-income status, traditional grant-based aid began to decline, and development finance institutions increasingly shifted toward commercial and near-commercial engagement with the private sector. This raised a practical question: who would serve as the interface for DFIs seeking economy-wide impact? While banks absorbed concessional debt, private equity emerged as the natural vehicle for deploying long-term risk capital into SMEs, innovation, and emerging sectors.

In this sense, PE/VC was not merely a financial innovation, but an institutional response to the gradual unwinding of the aid era. This global rethinking accelerated after the 2008 financial crisis, as donor countries and development finance institutions reassessed the effectiveness of traditional aid.

“Development finance was no longer only about aid,” recalls Shabda Gyawali of Dolma Impact Fund. “It became about finding solutions where traditional aid had fallen short—solutions that were effective, sustainable, and scalable.”

Nepal, emerging from conflict and prolonged political transition, offered both risk and opportunity. Yet equity capital faced deep cultural resistance. Entrepreneurs understood debt. Banks demanded collateral and personal guarantees. Equity, by contrast, implied shared ownership, transparency, and external oversight. Convincing promoters that an investor could be a partner rather than a threat took time. External shocks—the 2015 earthquake, the blockade, and recurring political instability—further delayed momentum. Risk capital survived, but it remained niche.

From Aid to Equity

Dolma Impact Fund’s experience illustrates both the promise and the limits of Nepal’s early private equity experiment. Fundraising began in 2012, and by 2014 Dolma had raised $36.6 million from European development finance institutions. Yet its first investment came only in 2016.

“The private sector understood loans, not equity,” Gyawali explains. “The idea that an investor would share both profits and losses was unfamiliar.”

Dolma’s first hydropower investment merged two small projects into a single company, introducing scale, governance discipline, and institutional shareholder agreements. The transaction challenged prevailing banking norms by demonstrating that institutional investors do not require personal guarantees.

Not all early investments succeeded. The e-commerce platform Sastodeal eventually failed, and the investment was written off. Yet even that failure mattered.

“It showed what early-stage risk looks like,” Gyawali says. “You don’t build ecosystems without failures.”

Private equity also introduced ESG standards to Nepal’s corporate landscape. For DFI-backed and impact-oriented funds, private equity is not only about deploying capital but about embedding resilience and governance into enterprise growth. Impact, in this context, is deliberate rather than incidental. Fund managers increasingly integrate ESG standards, gender inclusion, and climate-risk assessments into investment decisions, while working with portfolio companies on issues such as insurance coverage, operational resilience, and adaptation to climate shocks. This approach reflects a recognition that SMEs—often celebrated for job creation—are also among the most vulnerable to environmental and economic disruptions. Strengthening resilience at this level is not ancillary to returns; it is integral to sustainability.

At the transaction level, projects were assessed not only for financial returns but for governance quality, environmental compliance, and social impact. Flexible capital structures—convertible equity and preferred shares—began to appear where traditional bank financing was unavailable.

Despite these innovations, the ecosystem remained constrained by the absence of a domestic regulatory framework. Funds were structured offshore, and foreign investment rules did not recognize pooled fund vehicles operating within Nepal.

The SIF Turning Point

That changed in 2019, when Nepal introduced the Specialized Investment Fund Regulations. For the first time, private equity and venture capital were explicitly recognized within the country’s financial architecture.

“When the government introduced the SIF Regulations, it sent a clear signal that PE/VC had been formally accepted,” says Thapa. “That recognition mattered as much as the capital.”

Initial uptake was cautious. Global Equity Fund was the first to apply. Regulators hesitated, unsure how to supervise a new asset class. Merchant banks raised questions about role overlap and regulatory boundaries. Clarity emerged gradually. By 2021–22, the first licenses were issued. Lock-in provisions were clarified. Institutional investors began to engage. Momentum accelerated.

“After 2022, the number of funds, the size of their funds, and the volume of investments increased sharply,” Thapa says. “Today, Nepal’s domestic private equity market has raised around NPR 20 billion.”

A quieter but equally consequential shift is now visible beneath these headline figures. Nepali PE/VC fund managers are no longer focused solely on launching and deploying their first funds; several are actively preparing successor vehicles. Early SIF-licensed funds have moved beyond proof of concept to portfolio construction, disciplined deployment, and initial exits—bringing questions of continuity, track record, and institutional credibility to the fore. As Thapa observes, some domestic funds have already closed or are nearing the end of their first investment cycles, while others are confronting the harder task of raising second and third funds amid capital concentration, regulatory friction, and limited institutional participation. Dhruba Timilsina similarly notes that most SIF fund managers are now in transition—from deploying inaugural capital to building durable fund platforms capable of attracting repeat commitments. This evolution marks a structural turning point: Nepal’s PE/VC ecosystem is no longer defined by one-off funds, but by the emergence of managers seeking permanence, scale, and credibility across fund generations.

The speed of the transition has been striking. Between 2012 and 2024, SIF-licensed funds accounted for roughly 36% of all PE/VC investment in Nepal—nearly matching offshore FDI-backed funds, which took more than a decade to build their presence.

In 2024 alone, SIF funds dominated capital deployment, accounting for nearly three-quarters of all investment.

2024: The Breakout Year

The NPEA data makes clear that 2024 was not simply another incremental year. It marked a qualitative shift in scale, confidence, and participation.

Forty deals were closed during the year, the highest annual figure on record. Nine funds were active, including three new entrants deploying capital for the first time. Nepal Opportunity Fund–I and Reliable Private Equity Fund together accounted for nearly half of all transactions, underscoring the emergence of anchor investors capable of driving deal flow.

“The growth we’re seeing reflects regulatory clarity and institutional participation,” says Timilsina of Avasar Equity. “Bank credit alone cannot finance growth.”

Ticket sizes have increased significantly. Investments of Rs 200–500 million are now common in growth-stage companies and infrastructure-linked sectors. Capital is flowing into hydropower, solar energy, manufacturing, hospitality, information technology, and agro-processing.

The growing concentration of private equity capital in hydropower, solar energy, and hospitality reflects less a failure of imagination than a constraint of market structure. In an economy where secondary markets remain thin and IPOs constitute the primary exit pathway, capital naturally gravitates toward sectors with listing visibility, regulatory clarity, and scale. Smaller SMEs and innovation-driven firms often lack viable exit routes, making them difficult to support at larger ticket sizes without secondary markets. Until Nepal’s capital markets deepen and alternative exit mechanisms emerge, this sectoral skew is not an aberration—but a rational response to exit economics.

This pattern is borne out by the data. Sectoral data from the NPEA shows renewable energy—particularly hydropower—absorbing the largest share of capital, followed by ICT, manufacturing, and hospitality.

Capital with Structure

As capital volumes have grown, so too has the sophistication of investment structures. While common equity remains dominant, hybrid instruments are increasingly used to balance risk, returns, and promoter incentives.

“In early-stage and small-cap investments, assigning high valuations can be challenging,” says Timilsina. “But deploying large amounts of capital at low valuations can result in excessive dilution. Blended structures help align interests.”

Internationally, private equity funds routinely deploy a mix of equity, quasi-equity, and structured private credit, tailoring instruments to enterprise maturity and cash-flow profiles. In Nepal, however, regulatory frameworks still largely restrict funds to common equity and preference shares.

“The policy framework is evolving, but refinement is needed,” Timilsina says. “Greater alignment with international practice would significantly improve operational feasibility.”

Fund lifecycles present another challenge. SIF regulations require capital to be raised and deployed within relatively compressed timelines, while global closed-end private equity funds typically operate over ten years, with staged drawdowns and defined investment periods. In practice, capital is not deployed on day one; it is called as investment opportunities mature.

Taxation remains a further point of friction. The absence of a clear pass-through mechanism means income can be taxed at both the fund and investor levels, creating distortions—particularly for tax-exempt institutional investors. These structural frictions do not halt activity, but they raise costs and constrain flexibility as funds scale.

The Risk Gap

Despite record investment levels, Nepal’s PE/VC ecosystem continues to struggle at the earliest stages of enterprise development. “The highest risk lies at the pre-seed and seed stages,” says Sonam Tenzin of Team Ventures. “In Nepal, investors willing to take that risk are still relatively few.”

Founded in 2016, Team Ventures has invested in more than 20 companies across sectors ranging from solar energy and real estate to food delivery, artificial intelligence, and agro-processing. It has exited seven investments and achieved overall returns of around 15%.

“When we started, capital protection was our primary concern,” Tenzin says. “Now we see funds expanding into manufacturing and hospitality, which reflects a maturing market.”

Yet early-stage innovation remains underfunded. Unlike mature startup ecosystems, Nepal lacks both a broad cultural acceptance of failure and policy instruments—such as first-loss capital or co-investment facilities—that can absorb early risk. As funds grow larger, they naturally gravitate toward later-stage, asset-backed opportunities with clearer exit visibility, leaving a persistent financing gap at the innovation end of the spectrum.

Policy Meets Scale

As private equity scales, tensions with existing policy frameworks are becoming more pronounced. Larger funds increasingly gravitate toward hydropower, solar, and five-star hotels—sectors with visible IPO exit pathways. SMEs and impact-driven ventures risk being sidelined.

“Private equity is not only about risk capital,” says Siddhanta Raj Pandey of Business Oxygen. “It also provides technical support, ESG integration, and helps projects meet bankability requirements.”

Pandey argues that Nepal’s regulatory framework has not kept pace with market realities. Debt, mezzanine finance, and hybrid debt instruments are not yet permissible under existing rules. Foreign investment restrictions continue to limit development finance institution participation in agriculture and education—sectors with the greatest development impact.

“These restrictions undermine the very objectives policymakers claim to support,” Pandey says. “The ecosystem has grown up. Now policy must catch up.”

Tax policy presents similar challenges. The absence of pass-through taxation and the application of Section 57 of the Income Tax Act complicate fundraising and follow-on investments, particularly during Series A and Series B rounds. For growth-stage companies, this creates friction precisely when additional capital is needed to scale.

Exits and the Next Phase

Exits remain the ultimate test of any private equity ecosystem. In Nepal, IPOs and promoter buybacks dominate. Secondary markets are thin, and liquidity constraints persist.

“Ultimately, fund managers are judged by exits,” says Gyawali of Dolma Impact Fund. “Returns define track records.”

As more PE-backed companies approach listing, Nepal’s capital markets will face new pressures. For larger firms, domestic liquidity may prove insufficient, raising the question of dual listings and cross-border exits.

“Some companies are simply too large for Nepal’s market,” Gyawali notes. “Policy needs to anticipate that reality.”

Market participants argue that enabling dual listings would not only expand exit options but also improve valuation discovery and international visibility. Others suggest that permitting Nepali PE funds to invest abroad—mirroring Indian practice—could attract foreign limited partners by diversifying risk and returns.

What Needs to Change in the SIF Regime

The rapid rise of SIF-licensed private equity and venture capital funds has exposed a paradox at the heart of Nepal’s regulatory framework. The very regulations that unlocked domestic capital mobilization are now increasingly cited as constraints on the ecosystem’s next phase of growth.

At its core, the challenge is not regulatory hostility but regulatory incompleteness. The SIF framework was designed when Nepal’s PE/VC ecosystem was small, experimental, and largely donor-driven. It has since evolved into a market with cumulative investment of $174 million by end-2024, rising ticket sizes, and growing institutional participation.

Yet many underlying assumptions embedded in the regulation remain anchored in an earlier phase.

One persistent concern relates to the legal structure of funds. Under Nepal’s current framework, SIFs are typically established as companies. “In most global markets, funds are structured under trust frameworks or as limited-liability partnerships,” says Thapa of Global Equity Fund. “Investors expect their liability to be limited strictly to their capital commitment. In Nepal, that clarity does not yet exist.”

This absence of a dedicated trust law or custodian-based fund structure directly affects foreign limited partner participation, particularly for development finance institutions, pension funds, and sovereign investors whose mandates require strict legal certainty. Without explicit limitation of liability, Nepal struggles to compete with regional fund domiciles.

Equally significant is the restricted menu of permissible investment instruments. International private equity routinely deploys equity, preferred equity, convertibles, and structured private credit. Nepal’s regulatory framework remains narrowly focused on common equity and preference shares.

“Private equity is not only about buying ordinary shares,” says Timilsina. “International practice demonstrates the use of equity, quasi-equity, and structured instruments depending on risk profile and stage. Our framework needs to recognize that.”

The absence of regulatory clarity around fund-based private credit creates further ambiguity. While Nepal Rastra Bank appropriately regulates deposit-taking institutions, private credit extended by closed-end investment funds is fundamentally different from bank lending. Treating both under the same conceptual umbrella limits innovation and discourages instruments that could better align investor protection with enterprise growth.

Fund lifecycle alignment presents another constraint. Globally, closed-end private equity funds operate on ten-year horizons, with capital commitments drawn down gradually over three to four years. Under Nepal’s SIF regulations, funds face pressure to raise and deploy capital within compressed timelines, creating unnecessary operational strain.

Liquidation mechanisms pose similar challenges. Investments in unlisted companies are inherently illiquid, and exits do not always materialize neatly within a predefined timeframe. International practice recognizes in-specie distributions, where investors receive proportional ownership in portfolio companies if cash exits are not feasible at fund maturity. Nepal’s regulatory framework does not explicitly recognize such mechanisms, creating uncertainty at the end of a fund’s life.

Taxation remains another fault line. The absence of a clear tax pass-through mechanism means income may be taxed at both the fund and investor levels, even when investors themselves are tax-exempt.

“Without pass-through treatment, distortions arise,” Timilsina says. “Tax-exempt investors can end up indirectly bearing tax through the fund structure, undermining neutrality.”

These distortions are compounded by provisions such as Section 57 of the Income Tax Act, which can trigger tax liabilities during follow-on fundraising rounds. For growth-stage companies, this creates friction precisely when additional capital is required to scale.

Sectoral restrictions on foreign investment further complicate matters. Several impact-critical sectors, including agriculture and parts of education, remain on Nepal’s negative list for foreign investment. While domestic funds can invest, foreign limited partner participation is indirectly discouraged.

“Most DFIs are eager to invest in agriculture and education because that’s where impact is greatest,” Thapa says. “If investments are managed by Nepali fund managers, these restrictions should be reconsidered.”

Pandey echoes this view, arguing that current thresholds for foreign participation in agriculture are commercially unrealistic. “Agriculture contributes about 23% of Nepal’s GDP,” he says. “Yet foreign investment is effectively blocked by conditions that don’t reflect market realities. This undermines both impact and growth.”

The cumulative effect is not stagnation but friction. Funds continue to raise capital, deploy investments, and prepare successor vehicles. But without regulatory refinement, Nepal risks capping the ecosystem’s potential just as it begins to deliver scale.

Foreign LPs and the Next Phase of Growth

As Nepal’s private equity market matures, its future trajectory will increasingly depend on two interlinked factors: the ability to attract foreign limited partners and the availability of credible exit pathways. But scale will hinge just as critically on domestic institutions. The next phase of Nepal’s private equity evolution may depend less on entrepreneurial appetite than on institutional participation. Although budget speeches have repeatedly permitted banks, insurers, and statutory funds such as the EPF,

CIT, and SSF to allocate a portion of their portfolios to SIFs, regulatory misalignment has limited actual deployment. Capital charges on bank investments, conservative exposure caps for insurers, and the absence of clear implementation guidelines have kept vast pools of long-term domestic capital on the sidelines. Even modest adjustments—such as raising insurance exposure limits or operationalizing existing budget provisions—could mobilize hundreds of billions of rupees, transforming private equity from a niche asset class into a systemic pillar of capital formation.

Historically, development finance institutions were the primary source of foreign capital in Nepal’s PE/VC ecosystem. Funds such as Dolma Impact Fund demonstrated that DFI participation could crowd in local capital, introduce governance standards, and absorb early risk. As domestic SIF funds now dominate deal flow, the question has shifted from whether foreign capital is necessary to how it can be integrated without distorting the market.

“DFIs have both an interest in Nepal and a mandate to invest here,” Thapa says. “But Nepal’s FDI regulations were not designed with fund-based investment structures in mind.”

Under current rules, foreign investors are typically required to pre-declare sector, investment amount, and ownership structure—requirements that run counter to the pooled-fund model, where capital is allocated dynamically across sectors over time. While the SIF framework has opened the door in principle, operational clarity remains limited.

Exits remain the defining test. IPOs and promoter buybacks continue to dominate, steering PE capital toward IPO-ready sectors such as hydropower, solar, hotels, and manufacturing. Smaller SMEs and innovation-driven firms, where IPOs are less viable, struggle to attract later-stage capital.

A Market That Can No Longer Wait

Nepal’s private equity and venture capital ecosystem has crossed the point at which it can be treated as an experiment. With domestic funds now driving the bulk of capital deployment, private equity has moved from the margins of the financial system to its core.

That shift brings responsibility. The rise of SIF-licensed funds has demonstrated how regulatory clarity can unlock capital at scale. At the same time, it has exposed the limits of incomplete reform. Legal uncertainty around fund structures, restrictions on investment instruments, unresolved tax treatment, and sectoral barriers to foreign participation are no longer abstract policy issues. They have become binding constraints on a market that is already deploying significant capital and preparing for its next phase.

The risk today is not collapse, but stagnation. Without timely reform, Nepal’s private equity ecosystem could become locked into a narrow corridor—dominated by IPO-ready, asset-heavy projects—while innovation-led firms, early-stage ventures, and impact sectors remain chronically underfunded.

Private equity was introduced in Nepal to address a structural gap: the absence of long-term risk capital in an economy overly dependent on banks, collateral, and short-term credit. That gap has not closed; it has evolved. As funds scale and ticket sizes increase, the central question is no longer whether private equity can mobilize capital, but whether policy can accommodate complexity.

The coming decade will be decisive. If Nepal aligns its regulatory framework with global fund practices—by clarifying fund entity structures, broadening permissible instruments, adopting tax pass-through principles, and reopening critical impact sectors to foreign participation—it can entrench private equity as a durable pillar of economic transformation. If it does not, the market will still grow, but unevenly, leaving much of its developmental promise unrealized.

Private equity in Nepal has learned to take risk. The test now is whether the state is willing to do the same.

(This was the cover story of January 2026 issue of New Business Age magazine.)

Source: https://www.newbusinessage.com/news/46914/nepals-pe-vc-comes-of-age/

Siddhant Raj Pandey

Siddhant Raj Pandey